Reality vs. Conspiracy: The Actual Economic Influence of the Rothschild Family

Discover the real history of the Rothschild family, their banking empire, wealth-building strategies, global financial influence, and the facts behind common conspiracy theories.

ENTREPRENEUR/BUSINESSMANWEALTHY FAMILYEMPIRES/HISTORYBANKING/CASH-FLOW

Shiv Singh Rajput

7/18/202612 min read

Few financial dynasties have generated as much fascination, admiration, and controversy as the Rothschild family. For more than two centuries, their name has been associated with international banking, government finance, industrial expansion, and immense private wealth. At the same time, they have become the subject of countless conspiracy theories claiming they secretly control governments, central banks, financial markets, and even the global economy.

The historical evidence presents a far more nuanced picture.

The Rothschilds were undeniably among the most influential private banking families of the nineteenth century. They revolutionized cross-border finance, helped modernize sovereign bond markets, financed major infrastructure projects, and built one of history's first truly international banking networks. Their influence was significant because they became exceptionally skilled at moving capital across borders during a period when international finance was still developing.

However, influence should not be confused with absolute control.

Understanding the Rothschild family's actual economic impact requires separating documented financial history from speculation. This article examines how the family's banking empire was built, the mechanisms behind its success, its role in shaping modern finance, and why so many misconceptions continue to circulate despite a lack of supporting evidence.

The Origins of a Banking Dynasty

The story begins with Mayer Amschel Rothschild (1744–1812), a coin dealer and banker in Frankfurt, Germany. Unlike many bankers of his time, Mayer Amschel did not intend to build a large institution centered in one city. Instead, he created a decentralized international network that would become one of the greatest competitive advantages in nineteenth-century finance.

His five sons established banking houses in Europe's leading financial centers:

Frankfurt

London

Paris

Vienna

Naples

Although each branch operated independently within its local market, they remained closely connected through family ownership, constant communication, and shared financial interests. This structure allowed capital, information, and credit to move across borders far more efficiently than most competing banks.

In many respects, this network functioned like an early multinational financial institution decades before globalization became a common concept.

How the Rothschild Banking Network Actually Worked

The Rothschild system was not built on secret influence or hidden political power. Its strength came from solving practical financial problems that governments, merchants, and investors faced every day.

Cross-Border Capital Transfers

Before modern electronic banking, transferring money between countries was slow, expensive, and risky. Gold and silver often had to be physically transported across long distances, exposing shipments to theft, war, piracy, or delays.

The Rothschild banking houses solved this problem by maintaining large balances across multiple European cities. Instead of moving bullion every time a transaction occurred, they settled accounts internally between family branches.

This system offered several advantages:

Faster international payments

Reduced transportation costs

Lower security risks

Greater liquidity during financial crises

Efficient foreign exchange operations

This approach closely resembles today's correspondent banking system, where financial institutions settle international transactions through trusted banking partners rather than transporting physical currency.

Information as a Competitive Asset

One of the family's greatest advantages was information.

During the early nineteenth century, financial markets operated in an era before telegraphs, telephones, or digital communications. News often traveled only as fast as horses or sailing ships.

The Rothschilds invested heavily in:

Private courier networks

Shipping intelligence

Diplomatic contacts

Commercial correspondents

Government relationships

Receiving economic or political information even a few days earlier than competitors could significantly improve investment decisions in bond markets and currency trading.

Many conspiracy theories later exaggerated this information advantage into claims of secret political control. In reality, their network represented an early form of superior market intelligence rather than evidence of manipulation.

Sovereign Bond Markets

Perhaps the family's greatest contribution to modern finance was its role in government bond markets.

Throughout the nineteenth century, European governments frequently needed enormous amounts of capital to finance wars, infrastructure, debt restructuring, and public administration. Raising these sums from individual investors was a complex undertaking.

Rather than lending only their own money, the Rothschilds specialized in underwriting sovereign bonds.

The process generally worked as follows:

A government sought financing.

The Rothschild bank evaluated the government's creditworthiness.

The bank structured a bond issue.

Bonds were sold to investors throughout Europe.

Investors received interest payments while governments gained immediate access to capital.

This model resembles the underwriting services performed today by major global investment banks.

Their reputation depended heavily on maintaining investor confidence. A failed government bond issue could damage the family's credibility across multiple countries, making prudent risk assessment essential.

Financing the Industrial Revolution

The Rothschilds are often remembered as bankers, but a large portion of their wealth ultimately became invested in productive industries.

As Europe industrialized throughout the nineteenth century, enormous amounts of capital were needed for projects that governments and private businesses could not easily finance on their own.

The family directed investment into sectors that formed the backbone of industrial development.

Railways

Railroads were among the largest capital-intensive projects of the nineteenth century. Construction required financing for land acquisition, engineering, bridges, tunnels, locomotives, and rolling stock.

The Rothschild banking houses participated in financing railway expansion across several European countries, helping integrate regional economies and accelerate trade.

Rather than merely speculating on railway shares, they often acted as long-term financiers, providing stability during periods of rapid industrial growth.

Mining and Natural Resources

Industrial economies depended heavily on reliable supplies of raw materials.

The family's investments expanded into the following:

Coal mining

Iron production

Copper mining

Gold mining

Mercury extraction

These investments reflected a broader strategy of supporting industries that supplied the infrastructure necessary for economic expansion.

Government Infrastructure

Among the family's most famous transactions was the British purchase of the Suez Canal shares.

When the Egyptian government decided to sell its shares in the canal due to financial distress, the British government sought immediate financing to secure the strategically important asset.

The Rothschild banking house in London arranged the necessary funding within days, allowing Britain to complete the purchase quickly.

This transaction is frequently misrepresented online.

The Rothschilds did not own the Suez Canal, nor did they construct it. Their documented role was that of a financial intermediary providing short-term financing for the British government's acquisition of shares.

This distinction illustrates the difference between financing an asset and owning or controlling it.

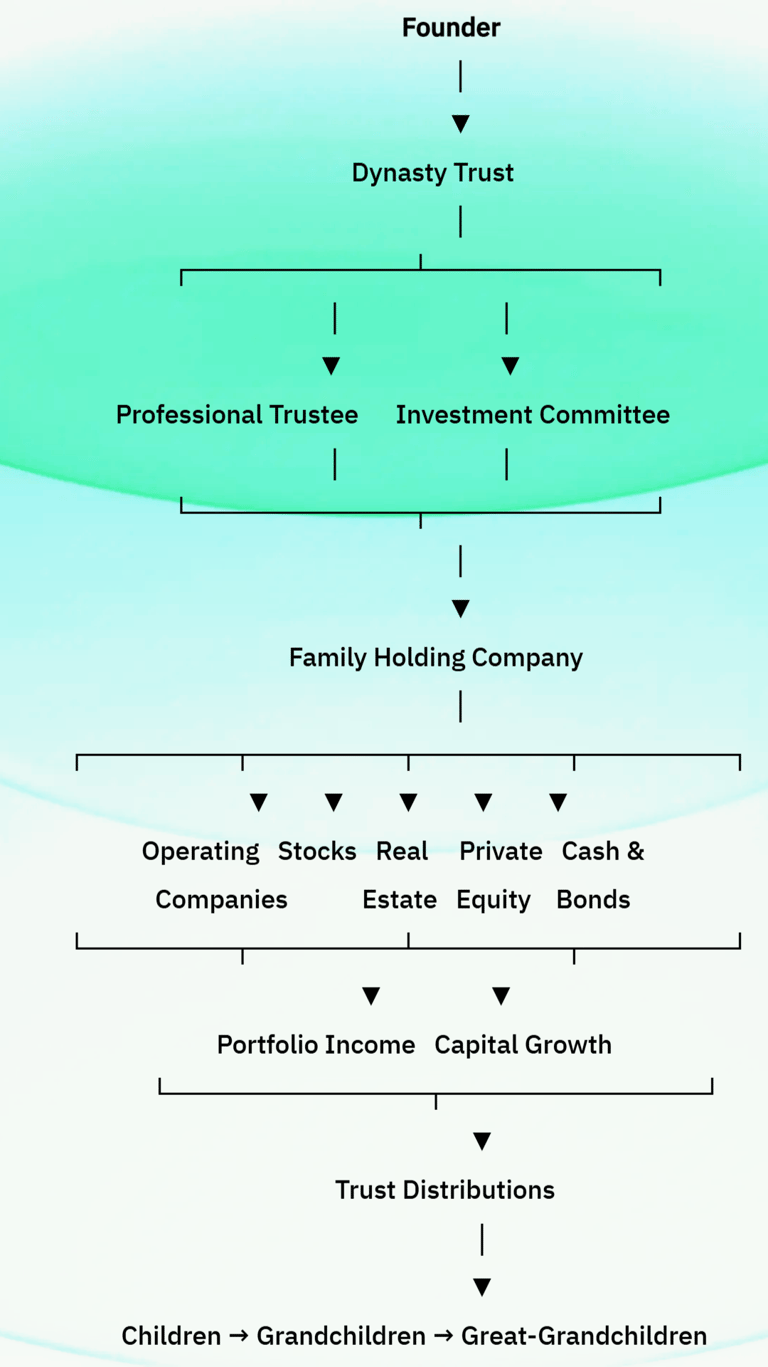

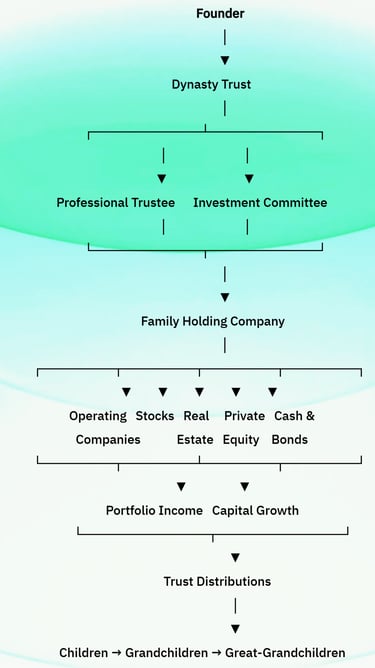

How the Family Preserved Wealth Across Generations

One of the most remarkable aspects of the Rothschild story is not simply how wealth was created, but how it was preserved.

Many fortunes disappear within two or three generations because heirs concentrate wealth in a single business, fail to establish governance structures, or neglect succession planning.

The Rothschild family adopted a much more systematic approach.

Family Partnerships

For much of the nineteenth century, the principal banking houses remained privately owned through family partnerships rather than publicly traded corporations.

This offered several advantages:

Long-term decision-making

Confidential business operations

Alignment of incentives

Centralized family governance

Without pressure from public shareholders demanding quarterly returns, investment decisions could focus on decades rather than months.

Geographic Diversification

Political instability frequently disrupted European economies. Wars, revolutions, changing governments, and currency crises could destroy fortunes concentrated in one country.

The family's multinational structure naturally diversified political risk. Operations in London, Paris, Vienna, Frankfurt, and Naples reduced dependence on any single government or financial market.

This geographic diversification remains a fundamental principle of institutional portfolio management today.

Diversification Across Asset Classes

The Rothschilds gradually expanded far beyond banking.

Their capital became distributed among multiple industries, including:

Government bonds

Commercial banking

Railroads

Mining

Agriculture

Vineyards

Real estate

Manufacturing

Precious metals

Infrastructure

Rather than relying on one dominant source of income, the family built multiple streams of long-term cash flow that could offset downturns in individual sectors.

Philanthropy as Institutional Legacy

Another often-overlooked aspect of the family's history is philanthropy.

Different branches of the Rothschild family established charitable foundations supporting:

Medical research

Public health

Education

Scientific research

Arts and culture

Environmental conservation

Historic preservation

While philanthropy did not drive the family's commercial success, it became an important mechanism for preserving reputation and creating long-term social influence.

Unlike conspiracy narratives, these activities are well documented through publicly established foundations and charitable institutions.

The Evolution of the Rothschild Business Model

The Rothschild business evolved alongside global finance. During the eighteenth century, the family primarily dealt in coins, precious metals, and foreign exchange.

By the early nineteenth century, sovereign lending and government bonds became the foundation of the business. As industrialization accelerated, capital shifted toward railways, mining, and infrastructure.

During the twentieth century, commercial banking gradually became more competitive as large national banks expanded and governments developed stronger financial institutions.

The Rothschild businesses responded by moving toward:

Merchant banking

Investment advisory

Wealth management

Corporate finance

Private equity

Asset management

This adaptability helps explain why the family remained financially relevant despite dramatic changes in global banking over more than two centuries.

Fact-Checking the Rothschild Family: Reality vs. Speculation

The Rothschild family's prominence has made it a recurring subject of conspiracy theories. Many of these claims originated in politically charged publications during the nineteenth century and have since spread through books, films, websites, and social media. Examining these assertions against historical records provides a much clearer understanding of the family's actual influence.

Myth: The Rothschilds own or control every central bank.

Reality: There is no historical or legal evidence supporting this claim. Modern central banks operate under national constitutions or legislative frameworks and are governed by public institutions, appointed boards, or statutory mandates. While private banks, including Rothschild firms, have historically advised governments or participated in sovereign bond markets, advisory roles do not constitute ownership or operational control.

Myth: The family secretly controls the global economy.

Reality: Today's financial system is too large and decentralized for any single family to dominate. Global capital is distributed among commercial banks, institutional investors, pension funds, sovereign wealth funds, insurance companies, multinational corporations, private equity firms, and public markets. The Rothschild businesses remain respected financial institutions, but they represent only a small portion of the overall global financial system.

Myth: The Rothschilds engineered wars for financial gain.

Reality: Historical records show that Rothschild banking houses financed governments through sovereign bond markets, just as several other European banking families did. Financing governments during wartime was a common banking activity in the nineteenth century. No credible archival evidence demonstrates that the family initiated or orchestrated wars to generate profits.

Myth: Their wealth exceeds that of all modern billionaires combined.

Reality: This claim has no documentary support. The family's wealth has been divided among numerous descendants and independent business interests over many generations. Modern estimates place many technology founders, industrial entrepreneurs, and investment managers ahead of individual Rothschild family members in publicly measurable wealth.

Myth: The family manipulates global currencies.

Reality: Foreign exchange markets today process trillions of dollars in daily transactions involving central banks, multinational corporations, commercial banks, hedge funds, and institutional investors. No evidence suggests that any single family possesses the capacity to control these highly liquid global markets.

The Decline of the Rothschilds' Relative Financial Dominance

One common misconception is that the Rothschild family's influence continued growing indefinitely. In reality, their relative dominance began to decline during the late nineteenth and early twentieth centuries, not because of financial failure, but because the structure of global finance fundamentally changed.

Several developments reshaped international banking:

The emergence of large joint-stock commercial banks with access to much larger pools of public capital.

The expansion of central banking systems, reducing governments' dependence on private banking houses for sovereign financing.

The growth of public stock exchanges, allowing corporations to raise capital directly from investors.

Two World Wars, which disrupted European financial networks and permanently altered international capital markets.

The rise of the United States as the world's largest financial center after the Second World War.

As financial markets became broader and more institutionalized, influence shifted away from individual banking dynasties toward multinational banks, public markets, pension funds, insurance companies, and later, global asset managers.

Rather than disappearing, the Rothschild businesses adapted by focusing on investment banking, corporate advisory, wealth management, and private capital, sectors where specialized expertise remained valuable.

How Modern Rothschild Businesses Operate Today

Many people assume the Rothschild family still functions as a single global banking empire. In reality, today's Rothschild-related businesses are independent corporate organizations operating under modern financial regulations.

Their activities generally include:

Mergers and acquisitions advisory

Wealth and asset management

Private banking

Corporate finance

Private capital advisory

Sustainability and ESG advisory

Long-term investment management

Like other international financial institutions, these businesses operate under banking regulations, anti-money laundering laws, financial reporting requirements, and oversight from national regulatory authorities.

Their role is comparable to other established merchant banks rather than a central authority within the global financial system.

How Historians Separate Fact from Financial Myth

Researching influential financial families requires distinguishing between documented evidence and popular narratives.

Professional economic historians typically rely on several categories of primary sources:

Government treasury records

Sovereign bond prospectuses

Corporate archives

Parliamentary proceedings

Central bank publications

Historical newspapers

Business correspondence

Probate and estate records

Academic research published by universities

Claims that cannot be supported by these sources remain speculation rather than established historical fact.

This evidence-based approach explains why reputable historians often reach conclusions that differ significantly from internet rumors or sensational documentaries.

The Rothschild Legacy in Modern Wealth Management

Although today's financial system operates on a vastly larger scale, several institutional practices that the Rothschilds helped popularize remain central to wealth management.

These include:

International portfolio diversification to reduce geopolitical risk.

Long-term capital allocation instead of short-term speculation.

Preserving liquidity during periods of market stress.

Building relationships based on credibility rather than transactional gains.

Investing across industries with different economic cycles to improve portfolio resilience.

Establishing structured succession planning to ensure continuity across generations.

Modern family offices, private banks, and institutional investors continue to apply many of these principles, even though they now operate within far more sophisticated financial markets.

Why the Rothschild Name Became Larger Than the Family Itself

Few financial surnames have evolved into cultural symbols in the way "Rothschild" has.

During the nineteenth century, the family became synonymous with international finance because its banking network was unusually visible and remarkably successful. Over time, this visibility transformed the family name into shorthand for wealth, banking, and financial influence in literature, newspapers, political commentary, and eventually popular culture.

As the family's historical reputation grew, public imagination often outpaced documented history. Complex economic events were sometimes simplified by attributing them to a single well-known financial dynasty, despite the involvement of governments, central banks, commercial institutions, and countless market participants.

Understanding this distinction is important because the Rothschild name today represents both a documented financial legacy and a broader cultural symbol, two concepts that are often mistakenly treated as the same thing.

Why Conspiracy Theories Persist

The persistence of Rothschild-related conspiracy theories reflects several historical and psychological factors rather than documented financial evidence.

First, the family's extraordinary success was unusual for its time. A single family maintaining influential banking operations across multiple European capitals naturally attracted public attention.

Second, much of private banking historically operated with confidentiality. Because client relationships and partnership agreements were not publicly disclosed, observers often filled gaps in knowledge with speculation.

Third, sovereign finance is inherently complex. Large government loans, bond issuances, and international capital movements can appear mysterious to those unfamiliar with how public finance functions.

Finally, historians have documented that many conspiracy narratives surrounding the Rothschilds incorporated longstanding antisemitic stereotypes, attributing broad global events to an imagined network of secret financial control. These narratives have repeatedly been discredited through archival research, financial records, and modern scholarship.

Lessons for Modern Investors and Wealth Builders

Although today's financial environment differs dramatically from that of the nineteenth century, several principles behind the Rothschild family's longevity remain highly relevant.

The first is diversification. Rather than relying on a single industry, geography, or source of income, they gradually expanded into complementary sectors that reduced overall portfolio risk.

The second is liquidity management. Maintaining access to capital during periods of economic instability enabled the family to finance opportunities when competitors struggled.

Another lesson is adaptability. The family's business evolved from currency exchange to sovereign finance, then to industrial investment, and later to wealth management and corporate advisory services. Their willingness to adjust to changing economic conditions helped preserve relevance across generations.

Equally important was governance. Long-term partnerships, structured succession planning, and professional management reduced the risks that often erode family wealth after the founding generation.

Finally, reputation proved to be one of their most valuable assets. Governments, institutional investors, and commercial clients repeatedly returned because confidence in a financial intermediary can be just as important as the capital it provides.

The Rothschild family occupies a unique place in financial history because its documented achievements are already extraordinary without the need for exaggeration.

They pioneered multinational banking networks; helped professionalize sovereign bond markets; financed railways, mining ventures, government borrowing, and major infrastructure projects; and demonstrated how diversified capital allocation and disciplined governance could preserve wealth across generations.

Their historical influence was substantial, particularly during the nineteenth century when private banking houses played a central role in European finance. Yet the evidence does not support claims that they secretly control governments, central banks, currencies, or the global economy.

Understanding this distinction is essential. The Rothschild legacy is best explained not by hidden power, but by financial innovation, international diversification, prudent risk management, institutional trust, and the ability to adapt to changing economic conditions over more than two centuries.

For historians, economists, and modern investors alike, the family's story offers a valuable lesson: enduring financial influence is built through sound institutions, strategic capital allocation, and long-term thinking, not through the extraordinary claims that have surrounded their name for generations.

FAQ's

Q: Who are the Rothschild family, and why are they historically significant?

The Rothschild family is a European banking dynasty that rose to prominence in the late eighteenth and nineteenth centuries. They built one of the first international banking networks, pioneered sovereign bond financing, and played a major role in funding governments, railways, mining ventures, and large infrastructure projects across Europe.

Q: Did the Rothschilds really control the world's economy?

No. While the Rothschilds were among the most influential private bankers of the nineteenth century, there is no credible historical evidence that they controlled the global economy. Today's financial system is decentralized and consists of governments, central banks, commercial banks, institutional investors, sovereign wealth funds, and public markets.

Q: What industries did the Rothschild family invest in?

Over more than two centuries, the family invested in a wide range of industries, including government bonds, banking, railways, mining, agriculture, vineyards, real estate, infrastructure, and wealth management. Their long-term diversification strategy helped preserve wealth across generations.

Q: Are the Rothschilds still wealthy today?

Yes. Various branches of the Rothschild family continue to own private investments and financial businesses. However, their wealth is divided among many descendants and is significantly smaller in relative terms than the world's largest publicly known fortunes held by modern entrepreneurs and investors.

Q: Did the Rothschilds own the Suez Canal?

No. The Rothschild banking house in London arranged financing that enabled the British government to purchase shares in the Suez Canal in 1875. They acted as financiers for the transaction but did not own or operate the canal itself.

Q: Why are there so many conspiracy theories about the Rothschild family?

Their exceptional financial success, international banking network, and historical privacy made the family a frequent subject of speculation. Over time, misinformation, political propaganda, and antisemitic narratives contributed to conspiracy theories that are not supported by credible historical evidence or financial records.

Q: How did the Rothschild family preserve its wealth for generations?

The family emphasized long-term planning through diversified investments, international operations, private partnerships, structured succession planning, professional management, and disciplined capital allocation. These strategies reduced risk and helped sustain wealth over multiple generations.

Q: What lessons can modern investors learn from the Rothschild family's history?

The Rothschilds' history highlights the importance of diversification, maintaining liquidity, managing risk, adapting to economic change, investing with a long-term perspective, and building strong governance structures. These principles remain fundamental to modern wealth management and institutional investing.

Subscribe To Our Newsletter

All © Copyright reserved by Accessible-Learning Hub

| Terms & Conditions

Knowledge is power. Learn with Us. 📚