How Dynasty Trusts Actually Work: The Legal Architecture of Generational Wealth

Learn how dynasty trusts actually work, including estate tax planning, GST tax, asset protection, trustees, holding companies, and the legal strategies families use to preserve wealth across generations.

ENTREPRENEUR/BUSINESSMANBANKING/CASH-FLOWA LEARNINGWEALTHY FAMILY

Shiv Singh Rajput

7/17/20269 min read

Dynasty trusts allow families to reduce or eliminate repeated estate taxation across multiple generations by transferring assets into an irrevocable trust that legally owns those assets for decades or even centuries. Because beneficiaries generally do not own the trust property directly, those assets can avoid being included in each generation's taxable estate while remaining professionally managed under carefully drafted legal rules.

Unlike ordinary inheritances, dynasty trusts are not simply about giving money to children. They are sophisticated legal structures designed to preserve ownership, manage investment decisions, protect assets from creditors, reduce transfer taxes where legally permitted, and maintain family governance over extremely long periods.

Why Dynasty Trusts Exist

Dynasty trusts emerged because wealthy families recognized that investment returns alone could not preserve fortunes across generations. Historically, large estates were repeatedly diminished by estate taxes, fragmented inheritances, family disputes, poor financial decisions, and forced sales of family businesses.

Rather than allowing ownership to pass directly from parent to child every generation, dynasty trusts were designed to create a continuous legal owner capable of surviving the death of individual family members. This allows businesses, investment portfolios, and real estate holdings to remain under unified ownership while future generations benefit economically without repeatedly restructuring ownership.

Dynasty Trusts Are Legal Systems, Not Investment Products

One of the biggest misconceptions is that a dynasty trust is a financial investment. It is not. A dynasty trust is a legal ownership framework.

Think of it as the operating system that controls:

ownership

taxation

distributions

governance

succession

asset protection

The investments inside the trust can continuously change while the legal structure remains intact for generations.

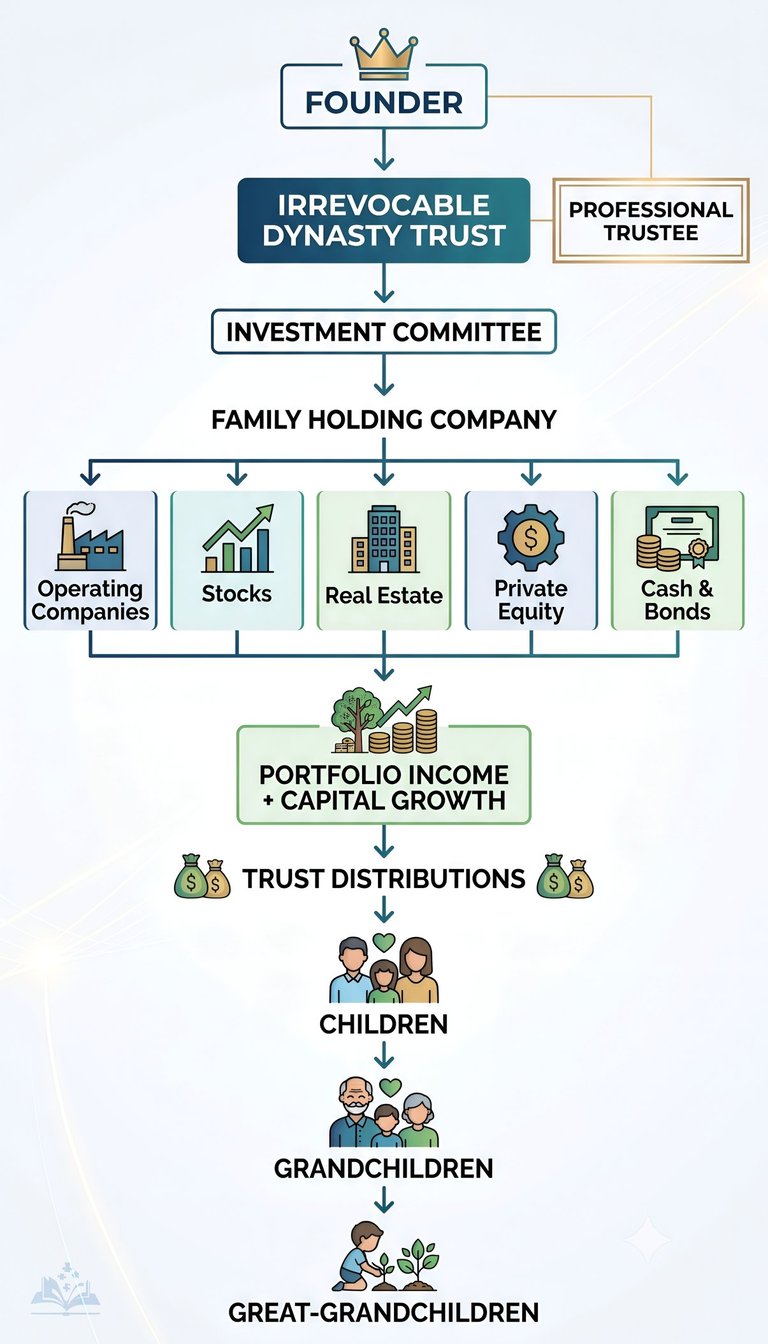

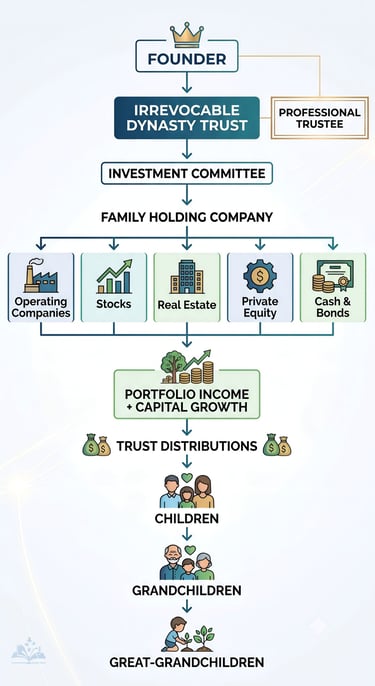

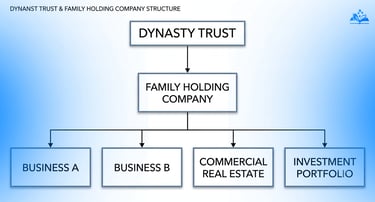

The Core Legal Architecture

A simplified structure typically looks like this:

Notice something important:

The family often does not personally own most of these assets.

The trust does.

That legal distinction is what makes the structure so powerful.

Step 1: Assets Move Into an Irrevocable Trust

The first stage is the transfer.

The founder contributes assets such as the following:

operating businesses

stock portfolios

commercial real estate

intellectual property

private equity

cash reserves

After transfer:

the founder generally cannot reclaim ownership

the trust becomes the legal owner

future appreciation usually occurs outside the founder's taxable estate

This is one of the most important mechanisms in estate planning.

Step 2: The Trust Never Dies

Individuals die. Trusts often do not.

Many U.S. states have modified or abolished the historical Rule Against Perpetuities, allowing certain dynasty trusts to continue for extremely long periods. Other jurisdictions impose different duration limits.

Instead of transferring ownership every generation:

Ownership stays inside the trust. This greatly reduces repeated wealth fragmentation.

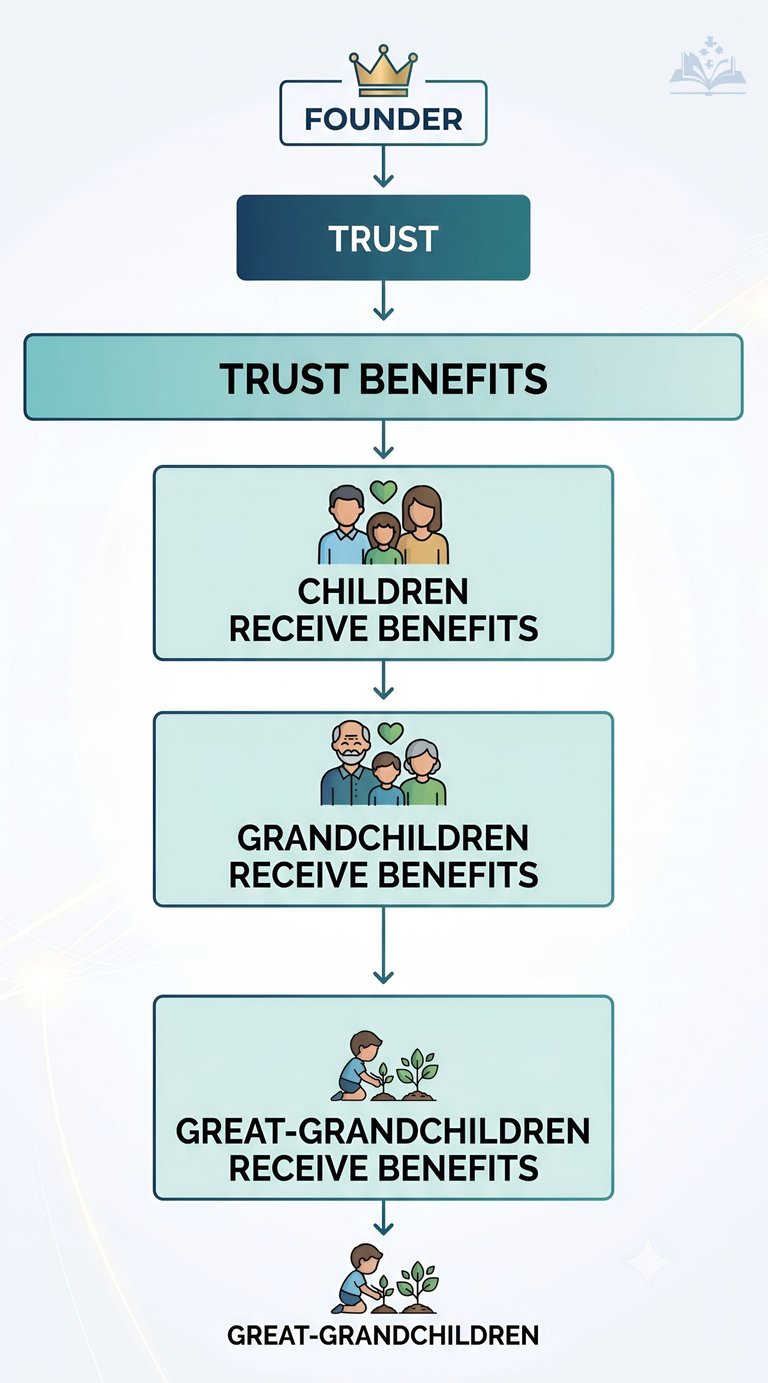

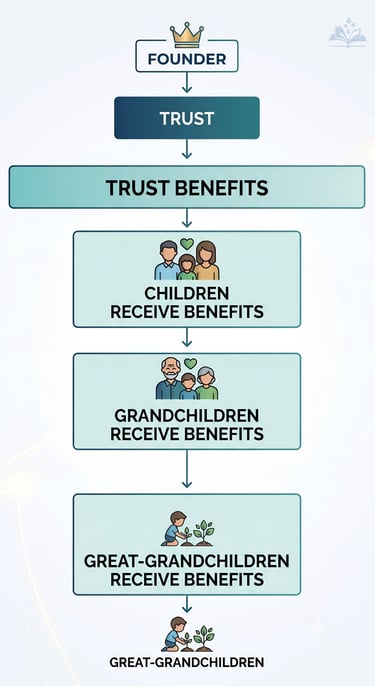

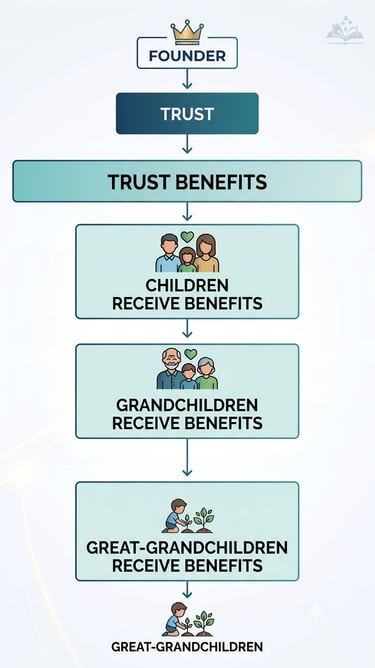

Step 3: Beneficiaries Receive Benefits Instead of Ownership

This is perhaps the least understood principle.

Beneficiaries often receive:

income

education funding

healthcare expenses

business capital

housing assistance

discretionary distributions

But they frequently never receive unrestricted ownership of the underlying capital.

That distinction protects wealth from:

lawsuits

divorces

creditors

bankruptcy

poor financial decisions

The capital continues serving future generations.

Step 4: Professional Trustees Control Administration

Ultra-high-net-worth families rarely rely on a single relative.

Instead they appoint:

trust companies

banks

fiduciary professionals

attorneys

accountants

Their responsibilities include:

enforcing trust terms

tax compliance

investment oversight

record keeping

beneficiary administration

The trustee owes fiduciary duties to the beneficiaries and must follow the governing trust document.

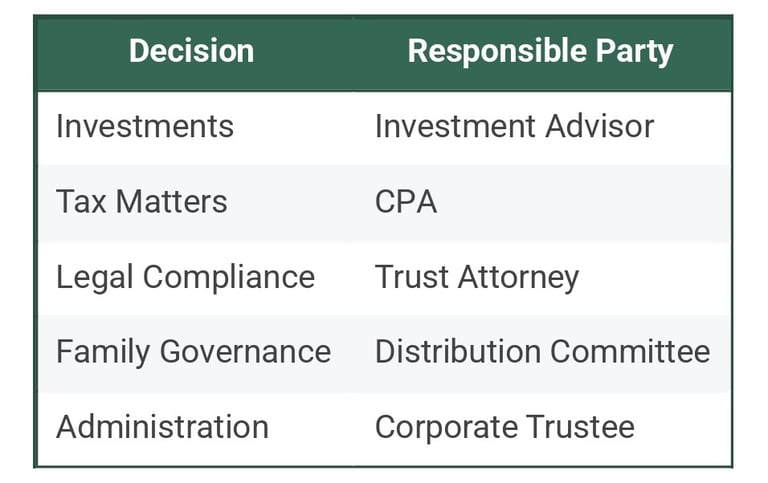

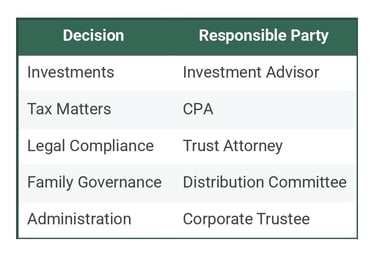

Step 5: Investment Committees Separate Family from Portfolio Management

Many large family trusts create investment governance systems.

Typical participants include:

portfolio managers

tax attorneys

economists

private equity specialists

independent advisors

This reduces emotional investing.

Capital allocation becomes systematic rather than personal.

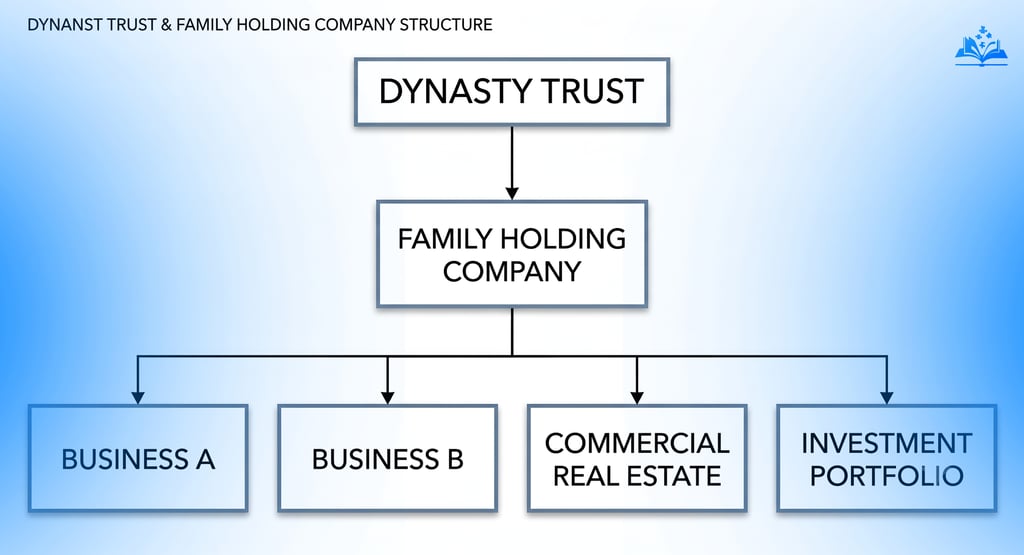

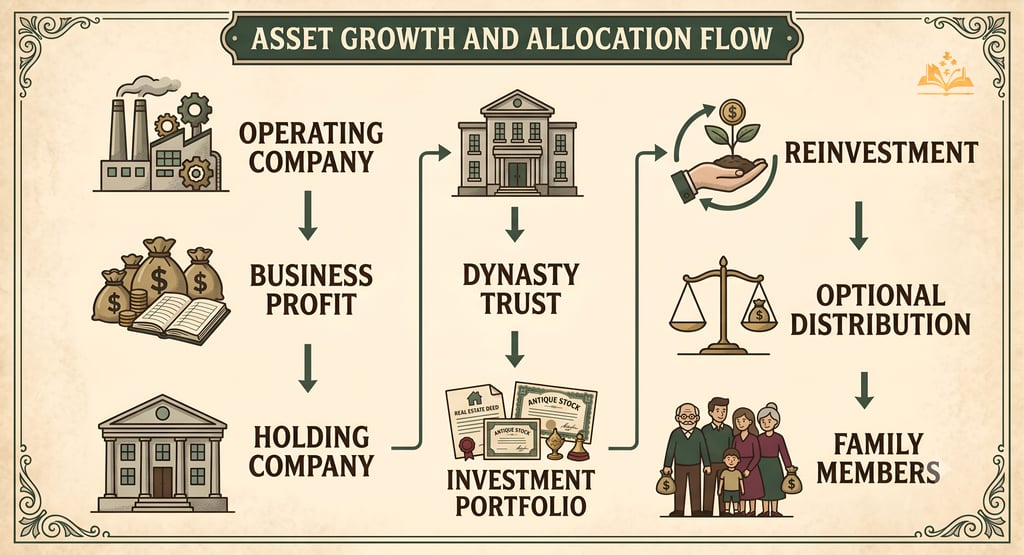

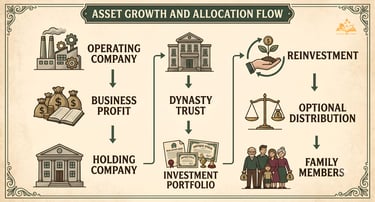

Step 6: Holding Companies Centralize Ownership

Instead of the trust owning hundreds of assets directly, it often owns a holding company.

Advantages include:

centralized governance

simplified accounting

easier succession

liability compartmentalization

efficient capital allocation

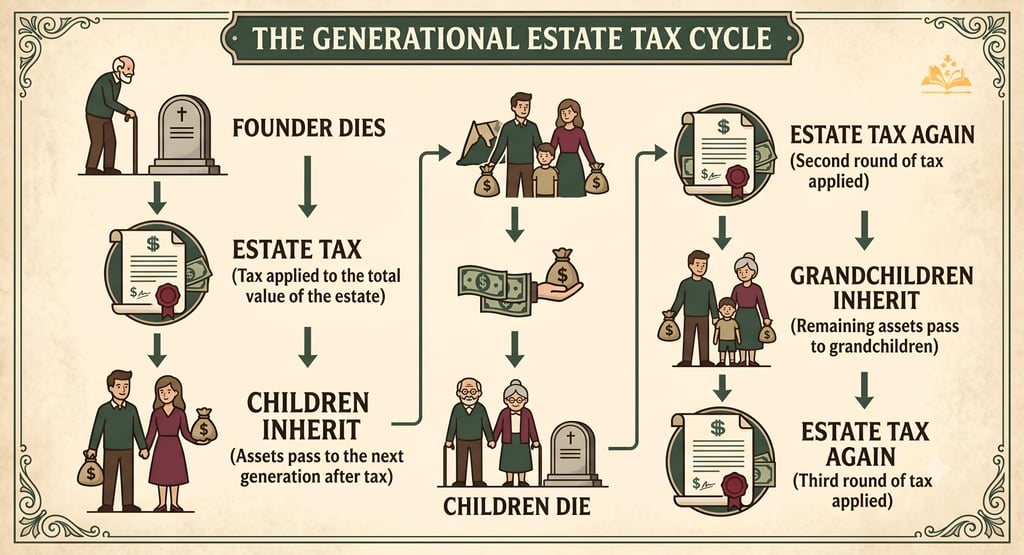

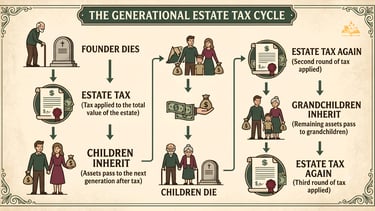

Why Estate Taxes Can Be Reduced Across Generations

Without planning:

With a properly structured dynasty trust:

Because the trust continues owning the property, properly structured assets may avoid repeated inclusion in each beneficiary's taxable estate, subject to applicable tax law, exemptions, and jurisdiction-specific rules.

This is the central mechanism that distinguishes dynasty trusts from ordinary inheritance planning.

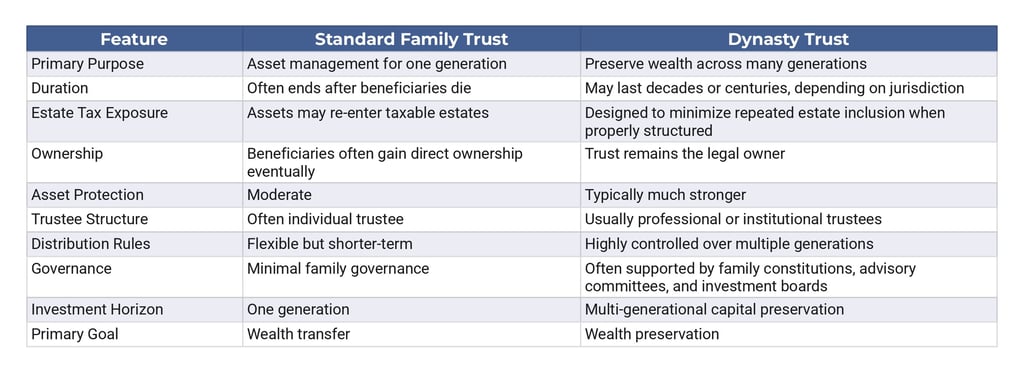

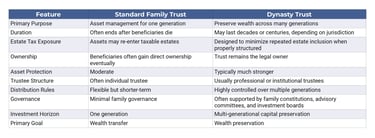

The Four Pillars of Multi-Generational Wealth Preservation

Beyond the Trust: The Broader Wealth Architecture

Dynasty trusts are rarely used alone. Large family wealth structures often integrate additional components.

Family Holding Companies

These centralize ownership across multiple businesses and investments while separating operating risk from family ownership.

Corporate Philanthropy

Private foundations and charitable entities can support long-term philanthropic goals, family governance, and succession education. They are not tax shelters in themselves and remain subject to extensive legal regulation.

Family Offices

Single-family or multi-family offices coordinate the following:

accounting

tax planning

investment reporting

risk management

estate planning

philanthropy

education for future generations

Global Banking Relationships

International families may maintain banking relationships across multiple jurisdictions for diversification, liquidity, and operational efficiency. These arrangements remain subject to applicable tax reporting, anti-money laundering, and cross-border regulatory requirements.

Why Wealth Usually Disappears by the Third Generation

Research and family office experience often identify recurring behavioral rather than investment failures.

Common causes include:

fragmented ownership

excessive distributions

poor governance

family conflict

lack of financial education

concentrated investment risk

absence of succession planning

Dynasty trusts address many of these governance challenges, but they are not a guarantee of perpetual wealth.

Generation-Skipping Transfer (GST) Tax

This is probably the biggest omission. Every article discussing dynasty trusts should explain it. Add after the Estate Tax section.

The Role of the Generation-Skipping Transfer Tax

The United States imposes a Generation-Skipping Transfer (GST) Tax to prevent families from avoiding estate taxes simply by transferring wealth directly to grandchildren or later generations.

A properly structured dynasty trust often allocates the founder's available GST tax exemption when funded. If structured correctly under applicable law, future appreciation inside the trust may continue benefiting later generations without triggering repeated GST taxation.

This exemption is one of the principal tax mechanisms that distinguishes dynasty trusts from conventional estate planning.

Spendthrift Clauses

This is another huge legal mechanism. After Beneficiaries Receive Benefits.

Spendthrift Provisions

Most dynasty trusts include spendthrift clauses.

These provisions generally prohibit beneficiaries from:

assigning future trust income

pledging distributions as collateral

selling future interests

allowing most creditors to seize trust assets before distribution

These clauses provide an additional layer of asset protection and help preserve trust capital from financial mismanagement.

How Money Actually Flows

Readers understand diagrams. They don't understand cash flow.

Example:

Distribution Standards

Readers never understand who decides. Explain it. Example:

Typical distribution standards include the following:

Health

Education

Maintenance

Support

Often called the HEMS Standard.

Trustees frequently use these standards to determine when discretionary distributions are appropriate while preserving trust assets for future generations.

Directed Trusts

Modern dynasty trusts increasingly use Directed Trusts. This deserves a section.

Example:

Instead of giving one trustee complete authority, responsibilities may be divided.

This specialization reduces conflicts of interest and allows experts to oversee their respective areas.

Trust Protector

Almost every sophisticated dynasty trust now includes one. Add after the Trustee section.

The Trust Protector

Many modern dynasty trusts appoint a Trust Protector, an independent individual or committee with limited oversight powers.

Depending on the governing document, a Trust Protector may be authorized to:

replace trustees

resolve administrative disputes

respond to changes in tax law

modify technical trust provisions where permitted

preserve the founder's long-term objectives

Unlike trustees, Trust Protectors generally do not manage investments directly.

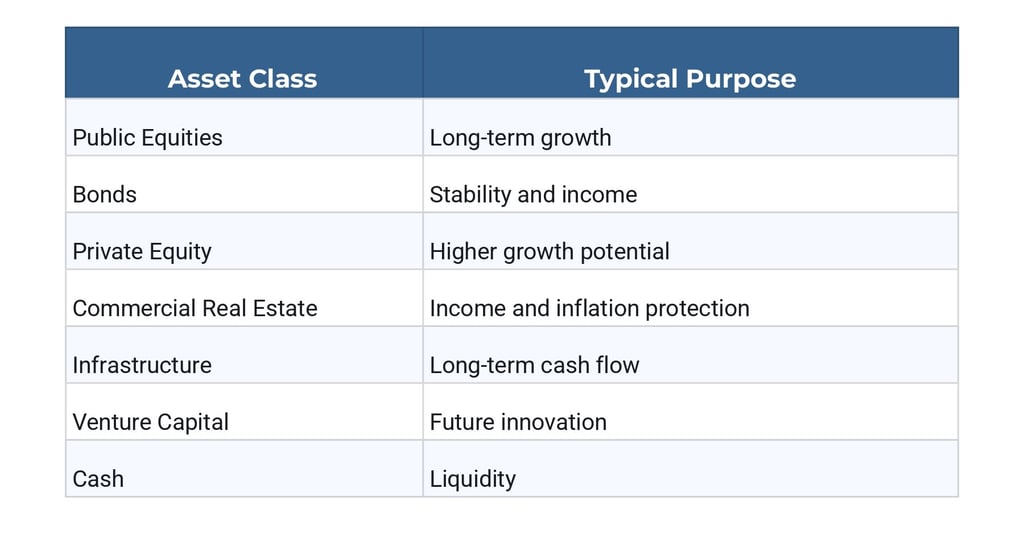

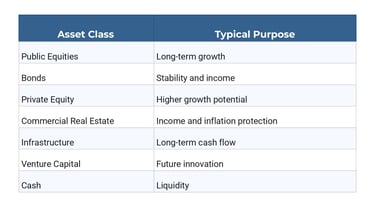

Asset Allocation Strategy

After Investment Committee. This is missing.

Example table:

Explain:

Large family trusts rarely depend on a single investment. Their objective is not to maximize returns every year but to create resilient portfolios capable of surviving recessions, inflation, geopolitical shocks, and changing market cycles.

Governance Documents

Most articles never mention this. Families often maintain documents beyond the trust itself.

Examples include:

Family Constitution

Investment Policy Statement (IPS)

Succession Plan

Philanthropic Charter

Family Employment Policy

Conflict Resolution Policy

These documents reduce ambiguity and provide consistent guidance as family membership expands over generations.

Jurisdiction Matters

After explaining the duration. Explain why South Dakota, Delaware, Nevada, Wyoming, and Alaska attract many U.S. dynasty trusts.

Topics include:

trust duration

state income tax

privacy rules

asset protection statutes

directed trust laws

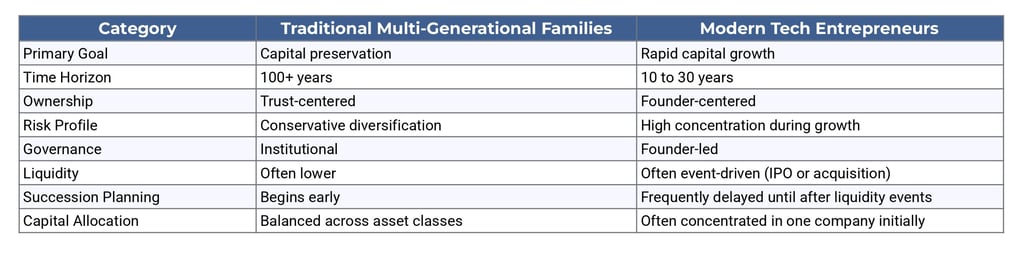

What Modern Wealth Builders Can Learn

Even entrepreneurs without billion-dollar fortunes can apply several enduring principles.

Separate Ownership From Management

A business owner does not necessarily need to personally own every appreciating asset indefinitely. Appropriate legal structures can improve continuity and succession planning.

Build Governance Early

Successful families often invest as much in decision-making systems as they do in investments.

Diversify After Liquidity

Many fortunes disappear because founders remain overly concentrated in a single asset after a major liquidity event.

Think in Decades, Not Years

Multi-generational wealth planning emphasizes resilience over short-term performance.

Educate Future Generations

Financial literacy, stewardship, and clearly defined governance are often as important as investment returns.

Key Takeaways

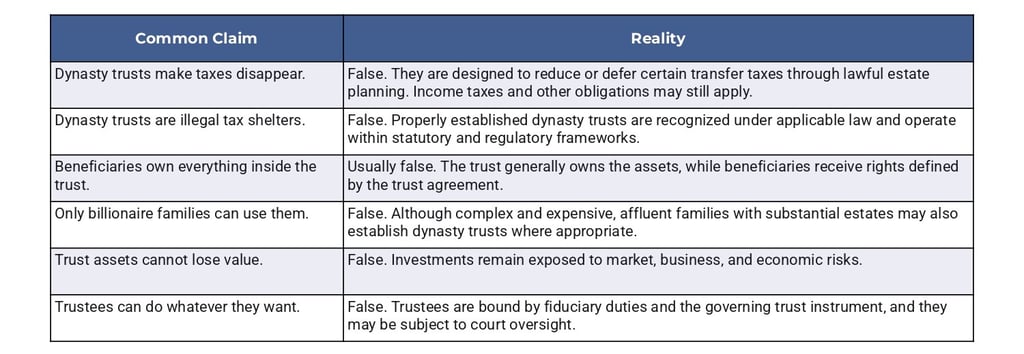

Dynasty trusts are not secret financial products or loopholes that magically create wealth. They are sophisticated legal frameworks that separate ownership from beneficial enjoyment, enabling long-term governance, professional management, asset protection, and more efficient intergenerational wealth transfer where permitted by law.

The families that preserve wealth for a century typically rely on more than successful investing. They combine carefully drafted trust structures, institutional governance, diversified asset allocation, disciplined succession planning, and long-term education. In that sense, the true architecture of generational wealth is not built on a single investment but on a durable legal and organizational system designed to outlast any one individual.

FAQ

Q: What is a dynasty trust in simple terms?

A dynasty trust is a long-term irrevocable trust designed to preserve family wealth across multiple generations. Instead of transferring assets directly to heirs every generation, the trust continues to own the assets while beneficiaries receive distributions according to predefined legal rules.

Q: How do dynasty trusts reduce estate taxes?

A properly structured dynasty trust may prevent trust assets from being included in each beneficiary's taxable estate. When combined with applicable estate and Generation-Skipping Transfer (GST) tax planning, this can reduce repeated transfer taxation across generations. The exact tax outcome depends on the governing jurisdiction, available exemptions, and the trust's structure.

Q: Who legally owns the assets inside a dynasty trust?

The trust itself is the legal owner of the assets. Beneficiaries generally have rights to receive distributions under the trust agreement but do not personally own the trust property.

Q: Can beneficiaries withdraw money whenever they want?

Usually not. Most dynasty trusts give trustees discretionary authority over distributions. Beneficiaries often receive funds for approved purposes such as:

Health

Education

Maintenance

Support (HEMS)

Some trusts allow broader distributions, while others are highly restrictive.

Q: What types of assets can be placed into a dynasty trust?

A dynasty trust may hold a wide range of assets, including:

Publicly traded stocks

Bonds

Private businesses

Commercial and residential real estate

Private equity investments

Venture capital holdings

Intellectual property

Cash and investment accounts

Family limited partnership interests

Q: Can a dynasty trust own an operating business?

Yes. Many wealthy families transfer ownership of privately held businesses into dynasty trusts through holding companies or family limited partnerships, allowing future business appreciation to occur within the trust structure.

Q: How long can a dynasty trust last?

That depends on local law. Some jurisdictions limit trust duration, while others permit dynasty trusts to continue for centuries or even indefinitely if statutory requirements are met.

Q: Who manages the trust's investments?

Investment decisions may be handled by:

Corporate trustees

Professional investment managers

Family offices

Investment committees

Independent financial advisors

Many modern trusts separate administrative duties from investment management.

Q: What is a Trust Protector?

A Trust Protector is an independent person or committee appointed to oversee certain aspects of the trust. Depending on the trust document, they may have authority to replace trustees, approve amendments, or respond to significant legal or tax changes without managing investments directly.

Q: Are dynasty trusts only for billionaires?

No. While they are most commonly associated with ultra-high-net-worth families due to their complexity and administrative costs, affluent families with significant estates may also use dynasty trusts as part of a long-term estate planning strategy.

Q: Can creditors seize assets inside a dynasty trust?

In many cases, properly drafted spendthrift provisions provide substantial protection against beneficiaries' creditors before distributions are made. However, the level of protection depends on applicable law, trust terms, and the specific circumstances of each case.

Q: Do dynasty trusts eliminate all taxes?

No. A dynasty trust is an estate planning tool, not a tax exemption. Trusts may still be subject to income taxes, capital gains taxes, property taxes, and other applicable taxes depending on the assets, jurisdiction, and trust structure.

Q: What happens if a trustee dies or resigns?

Most dynasty trusts include succession provisions allowing a replacement trustee to be appointed. This ensures the trust continues operating without interruption.

Q: Why do wealthy families prefer trusts over direct inheritance?

Because trusts can provide:

Long-term asset protection

Professional management

Controlled distributions

Greater privacy than probate in many jurisdictions

Succession continuity

Structured governance

Potential transfer tax efficiencies where legally available

Subscribe To Our Newsletter

All © Copyright reserved by Accessible-Learning Hub

| Terms & Conditions

Knowledge is power. Learn with Us. 📚