Digital Payment Intelligence Platform (DPIP): Revolutionizing Financial Transparency and Security

Discover how the Digital Payment Intelligence Platform (DPIP) is transforming the future of digital transactions through AI, fraud analytics, and real-time financial intelligence. Learn its features, benefits, use cases, and implementation challenges across banking, fintech, and governance sectors.

NEWS/CURRENT AFFAIRSSTOCK MARKETHARSH REALITY

Keshav Jha

6/26/20254 min read

The digital economy is evolving fast, with billions of digital transactions occurring daily across banking, e-commerce, fintech, and government sectors. This exponential growth brings with it challenges like fraud, financial crime, non-compliance, and lack of real-time insights. Enter the Digital Payment Intelligence Platform (DPIP)—a next-generation solution that leverages AI, big data, and real-time analytics to enhance payment visibility, fraud detection, compliance monitoring, and risk management.

What is a Digital Payment Intelligence Platform (DPIP)?

A Digital Payment Intelligence Platform (DPIP) is an AI-powered analytical framework designed to monitor, analyze, and secure digital payment ecosystems. It collects transaction data across digital channels (like UPI, IMPS, NEFT, wallets, and cards) and uses intelligent algorithms to:

Detect anomalies

Analyze user behavior

Identify fraud in real time

Provide data-driven insights to financial institutions and regulators

It’s a single-source payment surveillance tool developed to improve financial transparency, consumer protection, and systemic risk assessment.

Key Features of DPIP

Real-Time Transaction Monitoring

Monitors large volumes of financial transactions across digital payment channels for anomalies and red flags using AI/ML models.

Fraud Detection & Prevention

Uses behavioral analytics and predictive modeling to detect suspicious patterns such as spoofing, phishing, or mule accounts.

User Profiling & Risk Scoring

Profiles users based on past behaviors and assigns risk scores to transactions, helping identify high-risk actors before fraud occurs.

Data Integration Across Ecosystems

Aggregates data from banks, e-wallets, fintech apps, and payment gateways into a central intelligence hub.

Regulatory Compliance & Reporting

Provides dashboards, analytics, and reports to help institutions comply with KYC, AML, and regulatory requirements.

Anomaly Detection Engine

Identifies deviation from expected patterns using supervised and unsupervised learning models for deeper insights.

Technologies Powering DPIP

Artificial Intelligence & Machine Learning (AI/ML): For adaptive learning and real-time risk modeling

Big Data Analytics: To handle massive volumes of transaction data across diverse platforms

Cloud Computing: For scalability, faster deployment, and data accessibility

API Integration: Seamless data sharing with third-party apps, regulators, and financial networks

Blockchain (Optional Layer): For immutable record-keeping and traceability

Major Use Cases of DPIP

Banking Sector

Monitor high-frequency transfers

Prevent credit card fraud

Detect mule accounts

Fintech & UPI Platforms

Flag abnormal behavior (e.g., excessive UPI reversals)

Identify app misuse and merchant frauds

Regulatory Bodies (e.g., RBI, NPCI)

Oversee systemic transaction health

Alert on blacklisted accounts

Generate policy-grade reports

e-Commerce & Digital Retail

Ensure payment gateway safety

Reduce chargebacks and return frauds

Real-World Example: India’s DPIP by RBI

In early 2024, the Reserve Bank of India (RBI) proposed the development of a Digital Payments Intelligence Platform to oversee the country’s booming digital payments infrastructure. This centralized platform aims to:

Combat digital payment fraud

Improve interoperability of payment systems

Enable faster intervention in suspicious transactions

India’s DPIP is expected to become a model for global economies, especially in developing nations looking to build secure and scalable digital payment networks.

Challenges in Deploying DPIP

Data Privacy & Consent Management

Must comply with data protection laws like the DPDP Act and GDPR.Interoperability Between Systems

Requires standardization across diverse financial institutions.High Initial Investment

Setup costs, tech talent, and infrastructure may be prohibitive for smaller banks.Constant Algorithm Updates

AI models need to evolve with fraud techniques to remain effective.

Event-Driven Architecture (EDA)

DPIP platforms often operate on an event-driven architecture, where every transaction, login, or user action is treated as a discrete event. This allows the system to react instantly with

Trigger-based alerts

Microservice activation

Low-latency decisions

Federated Data Exchange Model

Instead of centralizing sensitive data, modern DPIPs utilize federated learning and edge computing to enable

Real-time fraud detection at source (bank/fintech app)

Cross-platform intelligence without exposing raw data

Privacy-preserving AI inference

Transaction Graph Analysis

DPIP builds graph-based representations of user behavior and relationships (like money flow between accounts), useful to:

Detect money laundering networks

Uncover synthetic identity fraud

Trace multi-hop payments and circular transfers

Cybersecurity Integration in DPIP

Threat Intelligence Fusion

Integrates with global threat databases (e.g., FS-ISAC, MITRE ATT&CK) to automatically:

Block known malicious IPs

Flag device fingerprint anomalies

Correlate phishing and malware trends with transaction patterns

Adaptive Access Control

The system can dynamically escalate security measures (like MFA or biometric re-authentication) mid-session, based on risk signals.

Institutional Integration Strategy

Plug-and-Play API Framework

Modern DPIPs provide:

RESTful APIs for easy embedding into banking apps or payment gateways

Webhooks for real-time fraud alerting

SDKs for mobile integration

Legacy System Compatibility

Using middleware and ETL pipelines, DPIPs can ingest data from:

Core Banking Systems (CBS)

SWIFT interfaces

POS terminals

Payment orchestration engines

Governance & Ethical Considerations

AI Explainability (XAI)

As regulations tighten, DPIPs are expected to comply with AI transparency norms, providing:

Audit trails for flagged transactions

Justification for risk scoring

Human-overridable decisions

Financial Inclusion Sensitivity

DPIP must differentiate novice digital users from fraudsters. Overzealous AI could lead to false positives that disproportionately affect underbanked populations.

Algorithmic Bias Mitigation

Regular fairness audits are necessary to ensure DPIP models don’t inadvertently target specific

Geographies

Socioeconomic groups

Merchant categories

Geopolitical & Economic Implications

National Security Use

Countries are exploring DPIP not just for fraud detection but also for:

Monitoring cross-border fund flows

Tracking crypto-to-fiat transactions

Combatting terrorism financing

International Financial Cooperation

DPIP platforms could form the backbone for:

Cross-border payment monitoring alliances (like G20 FATF frameworks)

Shared blacklist/whitelist registries across central banks

Data exchange under bilateral fintech treaties

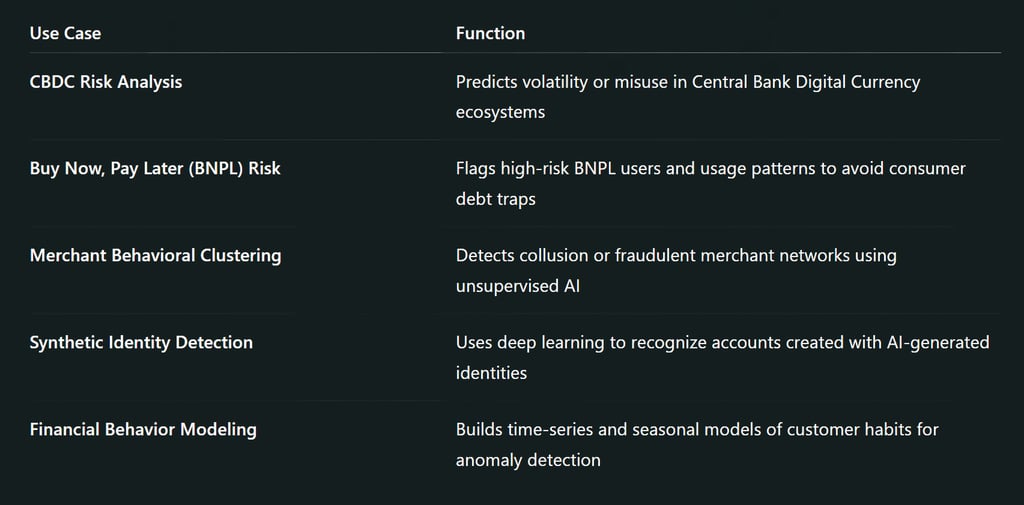

Emerging Enhancements in Pipeline

Quantum-Resistant Encryption for transaction data safety

Multilingual NLP Models for fraud cases in diverse regions

Voice Biometric Detection for fraud via call-center manipulation

Synthetic Data Simulation for stress-testing the platform under attack scenarios

Future Outlook: The Path Ahead

As digital transactions surpass physical cash globally, DPIP platforms will become the bedrock of financial security architecture. Their evolution will likely include

Integration with CBDCs (Central Bank Digital Currencies)

Self-learning fraud engines

Global interoperability standards

AI ethics and explainability modules

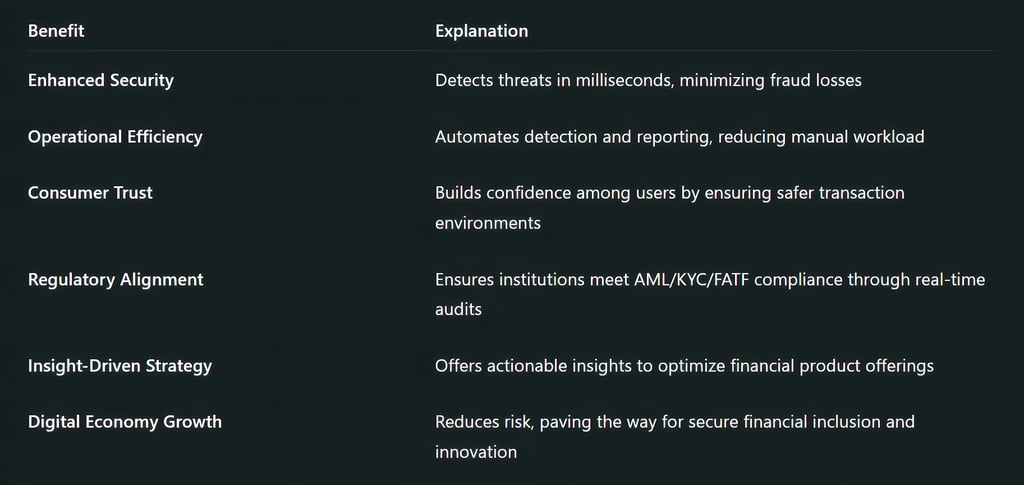

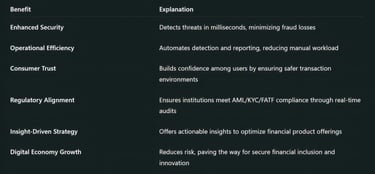

The Digital Payment Intelligence Platform (DPIP) represents a monumental shift toward secure, transparent, and intelligent digital financial ecosystems. As nations and financial institutions embrace the platform, it will empower users, protect the vulnerable, and fortify the digital economy with trust and intelligence.

FAQs

What is the role of AI in DPIP?

AI in DPIP enables real-time fraud detection, behavioral analytics, and predictive risk scoring, making it essential for modern financial intelligence.

Is DPIP only useful for banks?

No. It serves fintechs, e-commerce platforms, government regulators, and digital wallet providers.

How does DPIP ensure data privacy?

By implementing encryption, access controls, and aligning with legal frameworks like the Digital Personal Data Protection (DPDP) Act.

Can DPIP prevent all types of fraud?

While it drastically reduces risks, no system can offer 100% fraud prevention. However, DPIP significantly minimizes loss and improves response time.

What are the biggest challenges for DPIP implementation?

Data interoperability, regulatory alignment, infrastructure cost, and AI model updates are key challenges.

Subscribe To Our Newsletter

All © Copyright reserved by Accessible-Learning Hub

| Terms & Conditions

Knowledge is power. Learn with Us. 📚